Private equity is all grown up

When Martin Longchamps took over as head of private equity at Canadian pension fund Caisse de dépôt et placement du Québec in late 2022, he faced an unprecedented challenge: the institution’s allocation to private equity had reached 20 percent for the first time in its investment history, raising concerns over potential overallocation issues.

The country’s second-largest pension has been a seasoned private equity investor for almost half a century. However, it wasn’t until the last decade that the asset class began to account for a significant part of its investment portfolio: CDPQ’s private equity assets nearly doubled from 10.1 percent of its portfolio in 2013 to 20.1 percent in 2022. The upper limit for CDPQ’s allocation to PE was raised from 14.1 percent to 21.4 percent over the same period.

From the start of his tenure at CDPQ, Longchamps knew that his role would be different from the mantle taken on by his predecessors, each of whom had dedicated themselves to building and growing the pension’s PE programme. In Longchamps’ view, CDPQ’s private equity strategy has since reached a mature stage, particularly as it edges closer to its upper allocation threshold.

“If you look at the story of private equity at CDPQ, it was all about deployment up until 2020,” Longchamps tells Private Equity International. “Fast forward a couple of years later, private equity had performed well with great returns. Approaching the end of 2022, we found ourselves needing to address an overallocation issue.”

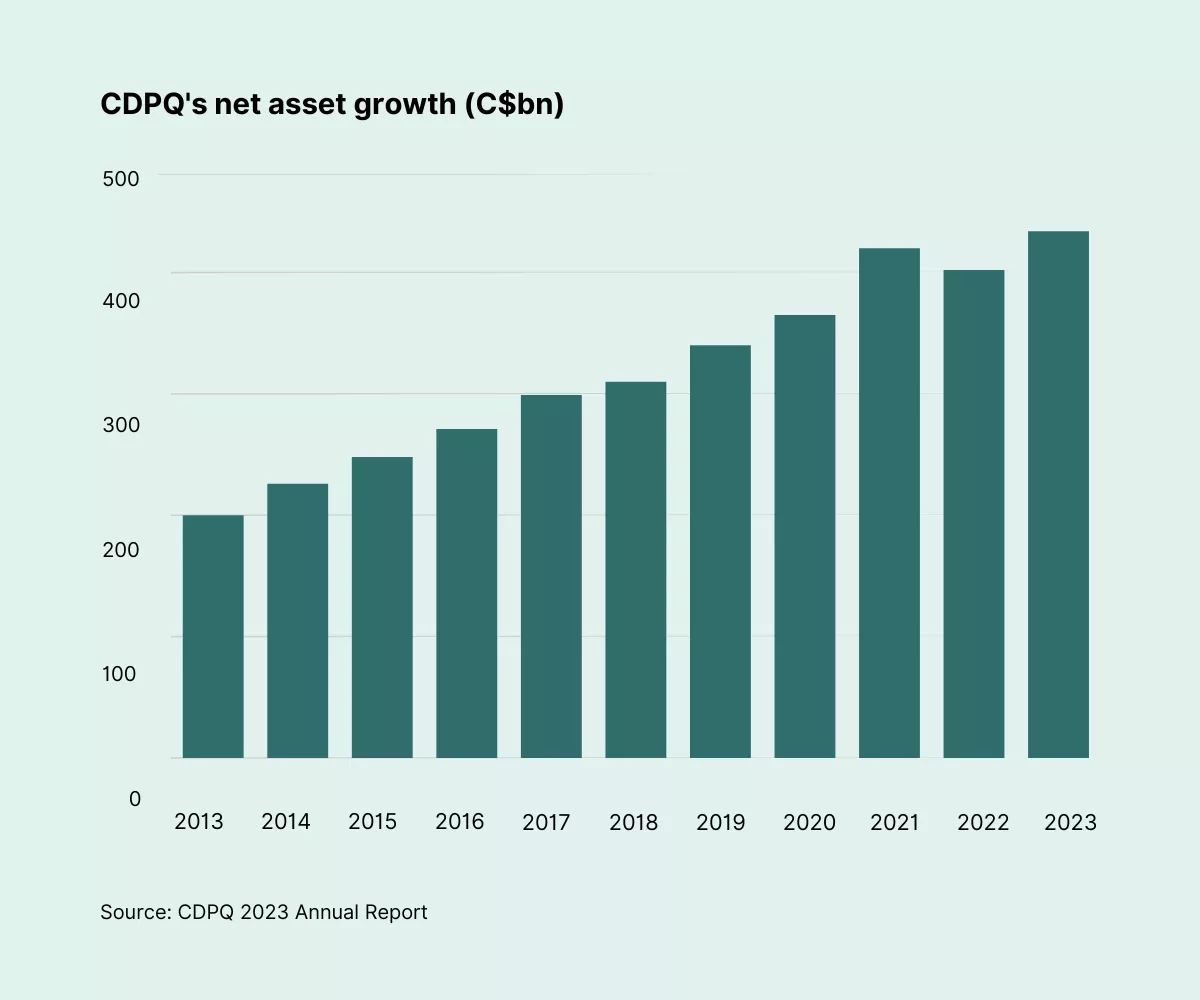

For the new helmsman of private equity at CDPQ, which has C$434.2 billion ($318.5 billion; €293.2 billion) in assets under management as of December, the priority is to steer the pension’s PE portfolio back to safe waters and ensure its allocation fits within the risk budgets of its 48 depositors.

“‘Don’t think about making new deals. Let’s make sure we get back to the allocation we should be.’ That’s the first thing I told my team,” Longchamps says.

A change of philosophy

When Longchamps took charge of CDPQ’s private equity business, its PE holdings were made up of 75 percent direct investments and 25 percent fund interests. Moving into 2023, he set a goal of reducing the pension’s PE allocation to 18 percent within three years, primarily by selling companies and exiting fund stakes via the secondaries market.

The shift required “a change of philosophy” for investment staff on the PE team, Longchamps adds. These professionals had been trained to spot top private companies and PE funds, rather than to sell their investments.

Divestments weren’t a major part of Longchamps’ past roles, either. Before joining CDPQ, he spent two decades at various investment firms across institutional and private sectors in Canada, where he oversaw deal sourcing, managed investment professionals and worked with executives at portfolio companies. Most recently, he served as head of origination and execution of private equity at the Public Sector Pension Investment Board, one of the largest Canadian public pension plans with C$244 billion in assets. During his five years at PSP Investments, he was responsible for identifying and executing co-investment opportunities with partner funds, as well as creating value for portfolio companies.

At CDPQ, however, Longchamps has found himself in a place where he needs to implement “a mindset of net negative deployment”.

“Given that we are at maturity, we need to sell more than we buy every year to avoid missing vintage years. That’s one of the [most] important changes that we needed to bring forward and deliver against,” he says. “Of course, the selling part is always the hardest, especially as the team had been built to focus on increasing investments rapidly.”

For the first four to five months of his term, Longchamps focused on uniting his team to embrace this transition within its private equity programme. He wanted to come up with a plan quickly, even though the market wasn’t favourable for sellers at the time.

“There is no rush to sell over the long term, but we [need] a plan for implementation and know what steps are required to bring the PE allocation back to 18 percent of the global portfolio.”

CDPQ wasn’t a stranger to the PE secondaries market prior to Longchamps coming on board. In late 2022, the system explored a sale of its PE fund stakes that was reported to be worth more than $1 billion, before ultimately deciding to hold off as markets deteriorated and pricing outlook appeared bleak, as affiliate title Buyouts reported at the time. Prior to that, the system had completed several large of-floads of its PE fund portfolios, including a sale of nearly $3 billion to Ardian in early 2022 and a sale of $1.3 billion to an investor group led by Goldman Sachs in 2018.

“Have people been able to sell in the past? Yes. [But] at that time, it wasn’t the focus of our team. It was more of an opportunistic approach and not necessarily driven by allocation issues, as we were in a ramp‑up phase,” Longchamps says.

“The worst thing that can happen at a pension fund is to miss a vintage”

Longchamps’ monetisation plan went smoother than he had anticipated. In 2023, his team generated C$9 billion in liquidity, including roughly C$6 billion from selling direct investments and receiving dividend recapitalisations, and around C$3 billion from selling PE fund stakes in the secondaries market.

One of the biggest direct sales that CDPQ made last year was the partial divestiture of USI Insurance Services, a US-based insurance brokerage and consulting firm that the pension acquired in an equal partnership with KKR in 2017. In September, CDPQ sold nearly two-thirds of its stake back to USI and KKR for C$1.5 billion, according to its 2023 annual report.

The C$3 billion divestment of PE fund stakes, meanwhile, comprised a strip sale of C$1.7 billion, which was finalised last August, and a full exit from a manager that no longer fit into CDPQ’s PE programme, which was completed in December, according to Longchamps.

The strip sale involved more than 60 international PE funds and co-investments, according to CDPQ’s annual report. The portfolio was considered high quality, with interests in funds from GPs including Genstar, CVC Capital Partners, Brookfield Asset Management, CD&R, Silver Lake, Veritas Capital and Stone Point Capital, Buyouts reported last year. Partners Group bought a large portion of the portfolio, sources told Buyouts.

“The secondaries space was very crowded when we hit the market. We decided to cut the trade in many transactions to expand the pool of buyers, and we were delighted with how it worked out,” Longchamps says. He adds that CDPQ was able to obtain an attractive price for its portfolio sale in the secondaries market.

Unlike other big LPs selling in the secondaries market last year, CDPQ didn’t allow buyers to cherry pick the best assets from its portfolio, according to a source familiar with the strip sale transaction. “It was ‘take it or leave it’,” the source says, adding that CDPQ was able to trade at a higher-than-expected price because it timed the market well. The process went so smoothly that Longchamps’ team managed to bring CDPQ’s PE allocation back to its 18 percent goal by the end of 2023, well ahead of the initial three-year target. What’s more, it was the first time in a decade that the institution’s PE allocation decreased relative to the total percentage of its overall AUM.

“Quite frankly, the success of our monetisation plan exceeded our expectations,” Longchamps says. He adds that monetisation “will always be part of CDPQ’s muscle”, given private equity’s ability to outperform in the long term.

“We have to bring velocity to the asset class,” Longchamps says. “Private equity is the asset class that takes the most risk at a pension fund. Therefore, it should deliver the highest return, which has certainly been the case.”

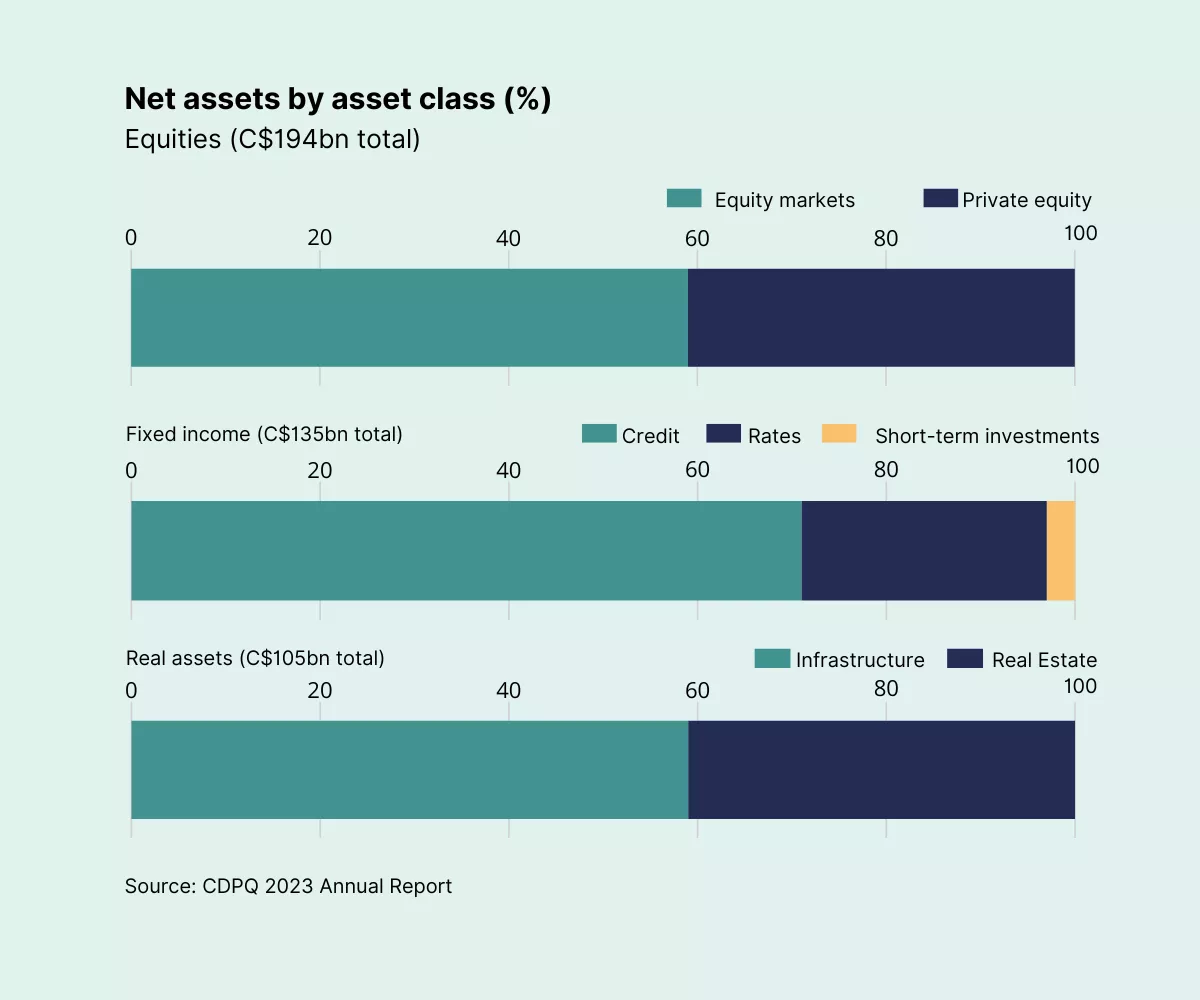

CDPQ’s net assets have increased by C$108 billion over the past five years, 38 percent of which stemmed from growth in its private equity portfolio, according to the pension’s 2023 annual report. Its PE investments achieved a 14 percent annualised return from 2018‑23, beating its benchmark by 1.6 percentage points. Over the same period, its PE portfolio delivered the highest annualised return across all asset classes, followed by infrastructure (9.5 percent), public equities (9 percent) and fixed income (1.7 percent).

In 2023, however, the pension’s PE portfolio only returned 1 percent, compared with an astonishing 17.7 percent generated by its public market counterpart. The annual report cites a sharp rise in interest rates and a slowdown in growth as factors that contributed to PE’s relative underperformance.

Even so, the recent uptick in public markets has worked in Longchamps’ favour: with PE’s performance lagging and his team selling off assets last year, they can now focus on deploying capital without concerns of overallocation in the near term.

“We are now back to our target allocation in 2024 and have regained our agility and flexibility to invest,” he says. “The worst thing that can happen at a pension fund is to miss a vintage.”

The alignment issue: How does CDPQ align with managers on its private equity fund sales?

For CDPQ’s GPs, accepting that they may be sold in the secondaries market doesn’t come naturally. However, the pension’s strip sale strategy seems to have worked well in creating an alignment of interests.

CDPQ offered only 5‑6 percent of its interest in funds involved in its partial portfolio sale last year, Buyouts reported. Longchamps says the strategy was well received by GPs because the pension keeps its vast majority of investments in the funds.

“Secondary sales are something we envision doing on an opportunistic basis to help manage allocation,” Longchamps says. “Our GP partners understand that it is now a tool for pensions to manage overallocation, and they want to help us get there. Additionally, the majority of what we sold was a strip of our portfolio, so we were not ending existing GP relationships. [Instead, we have retained] a collaborative approach.”

Peter Dubens, co-founder of Oakley Capital – one such GP – says the growth of the secondaries market is a healthy development and has made private equity more liquid. “If an LP wants to create liquidity by selling down a position in a group of GPs or a single GP while still being an investor, that’s just about rebalancing the portfolio,” Dubens tells PEI. “We would have no issue with that. It’s actually the beauty of the market.”

Nicolas Zerbib, co-president and CIO of Stone Point Capital, also supports LPs’ secondaries trades. “How LPs optimise their portfolio is their prerogative. Our job is to generate the best returns we can,” he says. “LPs have the right to transfer these stakes — it’s part of the free market that we live in.” Stone Point was among the managers involved in CDPQ’s strip sale last year, Buyouts reported.

Similarly, Jeff Rhodes, co-managing partner at TPG, says he doesn’t worry about CDPQ’s rebalancing exercise. “It’s very logical that with a new leader coming into the programme driving a new strategy, there would be some types of rebalancing… We are understanding of that.”

Expanding investments

Longchamps believes dealmaking activities will rebound in 2024, driven by companies’ pent-up demand for capital after a prolonged period of inactivity. “I think the second half of 2024 and 2025 [will] be a time where market [transactions] will come back in a significant manner. There are too many people sitting on the sideline waiting to sell their companies,” he says. “Pipeline and banking mandates to sell have never been greater. We see European dealflows improving significantly. We may have to wait post-election to see the pick-up in the US.”

Longchamps wants to seize this opportunity to make more strategic allocations, particularly through indirect investments. He aims to raise CDPQ’s fund investments from 25percent to 35 percent of its PE portfolio in the next five years.

“We decided that an integrated, partner-driven approach is the right one for us to create the velocity we need in our portfolio and to generate optimum levels of dealflow and returns,” he says. “Previously, we primarily made deals on our own and sometimes partnered with GPs, but they were not necessarily GPs we were in funds with. Fund investment acted more like a complementary strategy, and we are now fully integrated.”

A partner-driven approach will lead to more co-investment opportunities and help diversify CDPQ’s PE portfolio, he says, adding that the pension will rely on funds in sectors where it lacks internal expertise.

During the manager selection process, Longchamps says he values GP commitments because they serve as evidence of confidence and alignment of interests. The general rule of thumb is “the more, the better”. However, the absolute amount of commitment doesn’t matter as much as the relative significance of that commitment to the GPs themselves, he believes. “Some GPs are early in their life, so they don’t have that much capital to commit. In these cases, we look at how much it means to them.”

Rebecca Gibson, a partner at UK-based Oakley Capital — a €9 billion manager that CDPQ has been investing with in recent years — says the Canadian pension conducts detailed diligence on performance, distributions, unrealised return and realised returns.

“They are one of the more thoughtful and highly analytical teams that look at both current and past portfolios to understand what they can expect,” Gibson says.

CDPQ’s fund investment strategy has evolved over the past decade. While it was building out its PE programme, the pension was at one point working with more than 100 GPs. This number was pared down to about 20-plus in a reweighting of the portfolio towards direct investing, former head of PE Martin Laguerre told Buyouts in 2021.

The number of active GP relationships was further reduced to 15 last year, according to Longchamps. He aims to double the number to 30 in the next five years with a focus on mid-market managers. “When we evaluate new GP relationships, we always ask, ‘How can that relationship complement what we already have?’ What we are missing right now is a number of GP relationships in the mid‑market.” Mid‑market investments will help CDPQ accelerate exits, boost co-investments and gain access to a wider range of assets, he adds.

Longchamps says he believes returns are similar across large and mid-market GPs. However, the latter group has more exit options. This feature is particularly attractive as LPs and GPs continue to face distribution challenges amid a sluggish IPO and M&A environment.

His expectation for mid-market exits is supported by the data: the share of total PE exits made up by transactions under $500 million increased from 82 percent in 2010 to 90 percent in 2022, according to a mid-market PE report published by Morgan Stanley Investment Management in January.

Working with mid-market managers also fits into CDPQ’s plan to ramp up its co-investment activity. The institution’s sweet spot is deals of less than $500 million, which is more suitable

for mid-sized companies.

“We are developing a roster of mid-market GPs to execute co-investments with,” Longchamps says. “Our PE strategy lends itself better for deals in the mid-market right now versus mega-deals where you have to put in $500 million‑$1 billion.”

CDPQ has two co-investment strategies: passive co-investments for deals under $100 million and co-underwriting for deals between $200 million‑$500 million. “This combination aligns nicely with our strategy and provides the foundation for a diversifi ed PE portfolio,” Longchamps says.

The pension has already expanded its global footprint in the mid-market by working with TPG, New Mountain Capital, Harvest Partners and STG in North America, Cinven in Europe, Hanh & Co in South Korea, and Carlyle in Japan, according to Longchamps.

CDPQ’s plan to boost fund investments has been welcomed by GPs. Jeff Rhodes, co-managing partner at TPG – which has been partnering with CDPQ both on the fund and co-investment levels – says an increase in fund commitments will help better align the interests of LPs and GPs.

“Martin has done a great job of having a partner-orientated approach… that is focused on both fund commitments and co-investments in a flexible way. We feel very supportive as a partner to them,” Rhodes tells PEI.

Rhodes has known Longchamps since his time at PSP Investments, during which they served together on the governance boards of portfolio companies.

Nicolas Zerbib, co-president and CIO of Stone Point Capital, also started engaging with Longchamps when he worked at PSP Investments. Longchamps’ board governance approach has helped Stone Point enhance its partnerships with management teams, he says.

“Martin reads the boardroom well,” Zerbib says. “As a partner to us, he understands where the focus [is], where to lean in and where to engage. That takes a lot of experience and judgment.”

Deployment preference

When it comes to geographical exposure, CDPQ’s PE investments are mostly in North America (58 percent), followed by Europe (32 percent), Asia-Pacific (7 percent) and Latin America (3 percent), according to its 2023 annual report. The system increased its US exposure to 39 percent last year, a rise of 3 percentage points from 2022, while slightly decreasing its allocations to Canada and APAC.

Longchamps aims to boost CDPQ’s APAC exposure to 10 percent in the long term. His team is seeking to form partnerships with PE managers in Japan, South Korea, India and Australia. “These are good markets for buyouts,” Longchamps says. “We had more of a growth strategy in Asia before I arrived. Now, we want to devote more to the buyout strategy.”

CDPQ has already built fund relationships in China. “When they come [and] knock at our door for re-ups, we will decide what’s the best option for us. We are taking a wait-and-see approach,” he says. The pension has stopped making private deals in China and closed its Shanghai office last year amid increasing tensions between China and the West, according to media reports.

In terms of sector preference, CDPQ is mostly agnostic in its fund investments. “A lot of it depends on the strength of the GP. Some GPs are better in certain sectors than others,” Longchamps says.

For direct investments, it has dedicated teams covering technology, healthcare, business services and financial services, which are “promising and resilient areas”, according to its 2023 annual report. It will take an opportunistic approach in other sectors, such as energy, Longchamps says.

His belief that dealflow will pick up this year stems from a stabilising macro environment, which will likely bolster investors’ confidence in private markets.

“When I first took the job, I felt that we were going into uncertain years. However, we are now in a better place and the deals that I’m seeing so far provide an indication that they are going to be a good vintage,” he says.

“This year is all about execution – making sure we go back to the marketplace, start to invest again while continuing to actively monetise and manage our portfolio.”